When aspiring entrepreneurs embark on a search fund journey in Europe, they quickly discover that most of the literature on due diligence was written for a different market. The Yale and Stanford resources that form the backbone of search fund education were developed in the US, where the ecosystem has had forty years to mature and specialist advisors are well established. In Europe the picture is different. The model is newer, the advisor ecosystem is thinner and the legal mechanics vary significantly from one country to the next. This article describes what the due diligence process actually looks like for a European searcher, phase by phase.

What makes search fund due diligence different from other M&A processes

Due diligence in a search fund acquisition is fundamentally different from DD in private equity or large corporate M&A. Three factors define the SF context and shape every decision a searcher makes during the process.

First, budgets are limited. A searcher cannot afford to throw money at every question. This forces constant prioritisation between what is essential to know before closing and what would merely be nice to know. Every advisor engaged costs real money that reduces the deal budget.

Second, information quality is low. Most SF targets use QuickBooks or Excel, keep cash-basis accounts and have disorganised records with no existing data room. The seller has never been through a transaction before and does not know what a buyer needs. The searcher is often doing this for the first time too.

Third, both sides are inexperienced and emotional. The seller is selling their life’s work, often for retirement, and is prone to deal fatigue. The searcher has spent months or years getting to this point and is vulnerable to confirmation bias. Managing the seller relationship throughout DD is as important as the analytical work itself.

The two phases of due diligence

Search fund due diligence has two distinct phases with different goals, different tools and different levels of commitment from both parties.

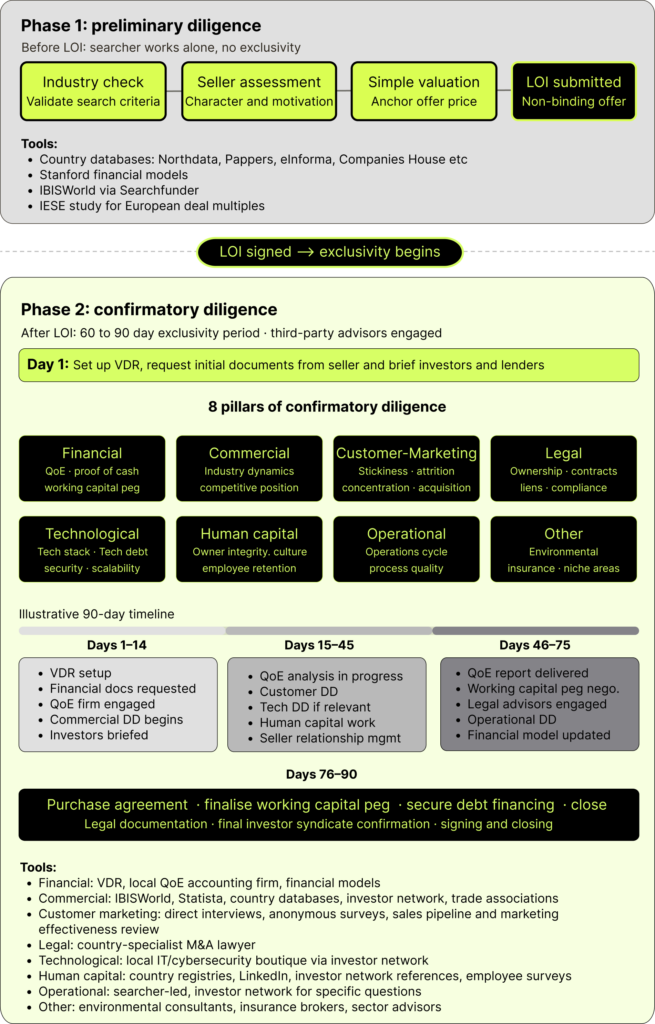

Phase 1: Preliminary diligence (pre-LOI)

Preliminary diligence happens before the LOI is submitted. The searcher has identified a promising target, had initial conversations with the owner and now needs to decide whether to make an offer and at what price.

Goals of this phase:

- Validate that the industry and business meet search fund investment criteria

- Assess seller character, motivation and genuine readiness to sell

- Build a simple valuation model to anchor the offer price

- Decide whether to submit a LOI and at what non-binding price

Key characteristics:

- No exclusivity period, so the seller will not hand over complete business information

- No third-party advisors engaged yet, the searcher works largely alone

- No formal timeline or clock pressure but real opportunity cost since time spent here diverts from sourcing

- Primary output is the LOI itself

Tools used at this stage: country databases for background research, financial modelling tools for a simple valuation model, industry research databases for commercial context, valuation comparables from public sources. No VDR is needed at this stage. QoE is not yet commissioned.

Phase 2: Confirmatory diligence (post-LOI)

Confirmatory diligence begins when the seller signs the LOI and grants exclusivity, typically for 60 to 90 days. This is the formal DD phase where the searcher goes deep across eight distinct workstreams with third-party advisors.

Goals of this phase:

- Make a clear yes or no decision on whether to acquire the business

- Validate or challenge the assumptions behind the LOI price

- Uncover red flags that could kill the deal or change the terms

- Build the final financial model for investors and lenders

- Finalise purchase price, deal structure and legal documentation

The VDR is set up on day one of the exclusivity period. It becomes the central secure repository for all documents exchanged between the seller, the searcher, their lawyers, their accountants, their equity investors and their lenders. For European transactions, GDPR compliance is a non-negotiable requirement, which is why European-native or EU-hosted VDR solutions are worth prioritising.

The eight pillars of confirmatory diligence

Financial: The most important and time-consuming pillar. Covers proof of cash, quality of earnings, tax review and working capital peg negotiation. Always requires an independent accounting firm and typically takes 4 to 5 weeks including producing the investor narrative. Quality of earnings is the core deliverable: it normalises historical EBITDA, identifies and validates add-backs and produces a pro forma normalised EBITDA figure that becomes the basis for the final purchase price and the lender’s credit decision. In a European context, Big Four firms are available but typically expensive for SF deal sizes. Specialist boutique transaction services firms with SME M&A experience are the practical option for most European searchers.

Commercial: Evaluates industry health, competitive position, market size, growth dynamics and barriers to entry. Uses secondary databases, industry reports and expert calls. Starts in preliminary diligence and extends into the first weeks of confirmatory.

Customer and Marketing: Analyses customer stickiness, attrition rates, concentration risk and contract quality. Also covers how the business attracts new customers, marketing effectiveness, customer acquisition costs and the sales pipeline. Involves requesting anonymised customer data from the seller and ideally conducting customer interviews, either directly or through a third-party customer diligence provider.

Legal: Reviews ownership structure, contracts, licenses, regulatory compliance, liens and past promises. Requires a specialist M&A lawyer with country-specific expertise. Most cost-effectively engaged towards the end of the exclusivity period once financial DD confirms the deal is proceeding. Legal mechanics differ materially across European jurisdictions in ways that affect deal structure, timeline and cost, making local expertise non-negotiable.

Technological: Assesses the company’s technology stack, third-party dependencies, cybersecurity posture, tech debt and scalability. Requires a specialist tech diligence advisor for any SaaS or technology-dependent business.

Human capital: Evaluates owner integrity and commitment to complete the sale, key employee retention risks, culture and company values. Conducted primarily by the searcher directly through conversations, observation and background checks.

Operational: Maps the full operations cycle from customer order to delivery, identifies bottlenecks and assesses process quality, safety controls and scalability. Conducted primarily by the searcher with occasional specialist support for manufacturing or industrial businesses.

Other: Industry-specific areas such as environmental compliance, insurance coverage, regulatory licences and any niche risk area that does not fit the other seven pillars.

Illustrative 90-day timeline

Days 1 to 14:

- Set up VDR and request initial documents from seller

- Begin financial diligence: request 3 to 5 years of financial statements, tax returns and bank statements

- Begin commercial diligence

- Engage accounting firm for QoE

- Brief equity investors and lenders on deal progress

Days 15 to 45:

- Financial diligence in full swing: QoE analysis, proof of cash, tax review

- Customer and marketing diligence: request customer data, begin interviews

- Tech diligence if relevant

- Continue commercial and human capital work

- Manage seller relationship actively

Days 46 to 75:

- QoE report delivered

- Working capital peg negotiation begins

- Engage legal advisors: ownership verification, contract review, regulatory checks

- Operational diligence: map the operations cycle

- Update financial model with QoE findings

Days 76 to 90:

- Legal documentation: purchase agreement and ancillary agreements

- Finalise working capital peg

- Secure debt financing commitment from lender

- Final equity investor syndicate confirmation

- Close

A note on the European advisor ecosystem

One honest reality for European searchers is that the specialist advisor ecosystem supporting search fund due diligence is less developed than in the US. In the US, specialist QoE firms, customer diligence providers and technology DD advisors have built practices specifically around search fund transactions. In Europe, most of these functions are either handled directly by the searcher, sourced through the investor network or delegated to generalist advisors who may not be familiar with the search fund model or its specific requirements.

This is not a permanent state. As the European search fund community grows, specialist service providers are beginning to emerge. But for now, the investor network remains the most reliable source of qualified advisor referrals in Europe, which is one of the strongest arguments for building a high-quality investor syndicate before the deal rather than after it.

This article is an educational overview of the due diligence process in a search fund acquisition. Every transaction is unique and requires qualified legal, financial and commercial advisors with relevant expertise in the applicable jurisdiction.